Share with your community!

Notice of Assessment: Understanding Canada Revenue Agency and Revenu Quebec NOA

As soon as you file a tax return, the Canada Revenue Agency (CRA) or Revenu Quebec issues a Notice of Assessment, commonly referred to as a NOA. This official document summarizes their tax decision and confirms whether the information you submitted has been accepted.

After filing a corporate tax return online, the Notice of Assessment becomes the reference point to validate your tax position, confirm the amounts assessed, and understand any adjustments made by the tax authorities.

Key Takeaways

- A notice of assessment is the official confirmation of tax payable or refundable after a return is processed by the CRA or Revenu Québec.

- A notice of reassessment is issued when changes occur following a correction, audit, objection, or new information.

- The notice number uniquely identifies your file and is required for objections and certain administrative steps with tax authorities.

- An arbitrary notice of assessment may be issued if no return is filed and can result in significant penalties and interest charges.

- You generally have 90 days from the date of the notice to file a formal objection if you disagree with the assessment.

What Is a Notice of Assessment (NOA)?

A Notice of Assessment (NOA) is an official document issued by the CRA or Revenu Quebec after processing a tax return. It confirms the tax assessment and indicates the amount of tax owing or refundable, the credits accepted or denied, instalments applied, and any adjustments made.

A notice of assessment applies to both individuals and corporations. For businesses, this is commonly referred to as a corporate notice of assessment, issued after the processing of a T2 corporate return federally or processing of a CO-17 return in Quebec.

The NOA summarizes the tax decision applicable to your personal return (T1 / TP1) or your incorporated business (T2 / CO-17). Its role is to validate the information submitted, confirm the final balance, and serve as official proof in the event of an audit, administrative request, financing application, or objection.

In practical terms, a notice of assessment allows you to:

- Verify the actual tax calculated by the CRA or Revenu Quebec.

- Confirm which credits and deductions were applied.

- Understand any adjustments made to your return.

- Retain a key tax document for financing or compliance purposes.

- Use it as a basis to correct a return or file an objection.

Notice of assessment in French is said avis de cotisation, in case you're in Quebec.

Notice of Reassessment (NOR)

A notice of reassessment is issued when the CRA or Revenu Quebec reassesses a previously issued notice of assessment. This can result from a taxpayer-requested correction, an accepted objection, an audit, or the receipt of additional information.

The notice of reassessment replaces the original assessment and details the changes made, along with their impact on the balance owing or refund. It should be reviewed carefully, as it may affect your tax obligations, interest charges, or objection rights.

Where to Find Your Notice of Assessment

You can download your notice of assessment online or receive it by mail, depending on your communication preferences with the CRA or Revenu Quebec.

How to Get it Through the Canada Revenue Agency (CRA)

Your Notice of Assessment is available via:

- My Business Account (for corporations)

- My Account (for individuals)

- Online Mail, if electronic correspondence is enabled

If the notice does not appear after standard processing times, your return may still be under review. In such cases, it is advisable to verify the status or contact the CRA.

How to Get it Through Revenu Quebec

In Quebec, Notices of Assessment are available through:

If your NOA is lost, Revenu Quebec allows you to request a copy directly through your online account or by phone. For more information, consult Revenu Quebec's official page on the notice of assessment.

To receive your notices more quickly and avoid postal delays, activating electronic correspondence is strongly recommended. Without this option, notices are sent by mail, which can lengthen processing times and make it more difficult to store and manage your tax documents, especially when multiple notices are issued over the years.

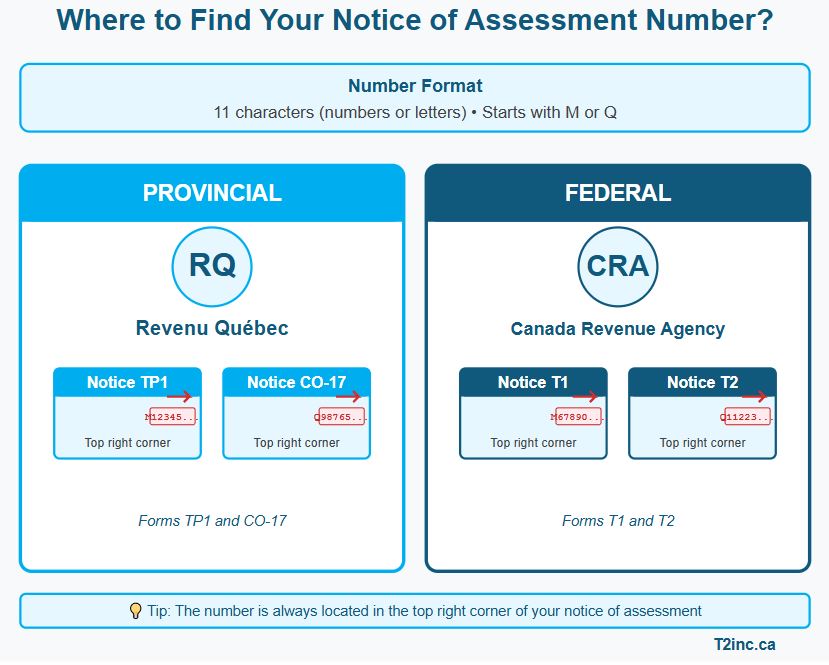

How To Find Your Notice Of Assessment Number

Your NOA number is made up of 11 characters, letters and/or numbers, and usually begins with M or Q. At the provincial level (Revenu Quebec), it appears in the top-right corner of TP1 and CO-17 notices. At the federal level (CRA), it is located in the top-right corner of T1 and T2 notices.

Keep this number in a safe place. It may be required to confirm your identity, respond to an audit, or file a formal objection with the tax authorities.

Understanding Your Federal Or Provincial Notice Of Assessment

A notice of assessment may seem complex at first, but its sections always follow the same structure. Each one provides key information to help you verify the tax assessment and anticipate your obligations.

1. Identification number

Located at the top of the notice, this unique number allows the tax authorities to locate your file. It is required to file an objection or respond to a request for information.

2. Amount owing or paid

This section shows whether you owe an amount, are entitled to a refund, or have a zero balance. Any interest or penalties are also listed. For businesses, any unpaid balance begins to accrue interest as of the due date.

3. Refund (if applicable)

If you paid more tax than required, the notice of assessment specifies:

- the refund amount;

- sometimes the expected deposit date; and

- if applicable, the portion applied to a prior balance.

For a corporation, the refund may result from a tax credit, an overpayment of instalments, or a favourable adjustment, and can be reinvested in the business.

4. Tax credits and adjustments

This section outlines the tax credits and deductions assessed, as well as any corrections made by the tax authorities.

- On a personal notice (T1 or TP1), you will see the personal credits applied (for example, GST credit, medical expenses, education) and, if applicable, credits that were denied with an explanation.

- On a corporate notice of assessment (T2 or CO-17), this section may list accepted or denied corporate tax credits, along with adjustments made to schedules.

You may also find amounts carried forward to future years, such as losses or unused credits. For business owners, this section helps confirm which credits were actually applied (for example, SR&ED, innovation, investment credits) and understand the changes made to your return by the CRA or Revenu Quebec.

5. Explanations for adjustments

When corrections are made, the notice includes a summary of the changes, sometimes accompanied by codes or references. Common reasons include:

- added or corrected income;

- a credit deemed ineligible;

- instalments applied differently;

- a corrected data entry error; or

- missing supporting documents.

If an adjustment seems inconsistent, compare it with your return, slips, and receipts before contacting the CRA or Revenu Quebec or consulting a professional.

Be Careful With An Arbitrary Notice Of Assessment

An arbitrary notice of assessment is issued when the Canada Revenue Agency or Revenu Quebec assesses your taxes without having received your tax return.

In this case, the assessment is based on partial or third-party information and does not take into account your actual expenses, depreciation, or tax credits. The result is often a significantly overstated tax bill, to which daily interest, late-filing penalties, and sometimes swift collection actions are added.

Filing a return after an arbitrary notice of assessment

In most cases, filing a tax return after receiving an arbitrary notice of assessment allows the estimated amount to be corrected. Submitting the missing returns—T2 at the federal level and CO-17 in Quebec—is the first step toward obtaining a reassessment based on your real financial figures.

That said, this option depends on the reassessment deadlines.

- At the federal level, the normal reassessment period is generally three years, sometimes four depending on the corporation. If the year is still open, the CRA can recalculate the assessment. Once this period has expired, the CRA is no longer required to correct the estimate, even if it is clearly too high.

- Revenu Quebec, on the other hand, is generally more flexible and more often agrees to adjust older years when the provincial return is eventually filed.

In all cases, the faster you act, the more you limit interest and penalties and the better your chances of a favorable revision. When an arbitrary notice of assessment affects a business, acting without delay is critical.

How to Dispute a Notice of Assessment from the CRA or Revenu Quebec

You can dispute a notice of assessment if you notice an error. This formal process lets you request a review of the tax assessment issued by the CRA or Revenu Quebec. Before disputing, make sure the discrepancy comes from the tax authority and not from an error in your own return.

Steps to follow:

- Review your return and slips.

- Identify the adjustment that seems incorrect.

- Correct your return online if the mistake is yours.

- File a notice of objection if the issue comes from the tax authority's assessment.

- Respect the applicable deadlines, usually 90 days from the notice date.

If the dispute is accepted, it can lead to the issuance of a notice of new assessment (the ADNC we mentioned earlier), which will replace the original notice.

T2inc.ca Supports You With Your Tax Obligations

If an amount differs from what you expected, take the time to review the NOA in detail. Most of the time, an explanation is already provided. And if something seems inconsistent or requires adjustment, don't hesitate to request clarification from the CRA or Revenu Quebec, or to consult a professional.

At T2inc.ca, we understand that corporate taxation can quickly become complex. If you want to file your T2 corporate tax return at the federal level, or file your CO-17 provincial return with a thorough and professional service, contact the T2inc.ca team. We can help you understand your tax obligations and manage your filings clearly, efficiently, and with confidence.

FAQ – Notice of Assessment in Canada

What is a CRA pre-assessment review?

A pre-assessment review is a preliminary examination conducted by the CRA before issuing the official notice of assessment. This process, which typically takes place from February to July, allows the authorities to verify certain deductions or credits claimed on your return. If your return is selected, the agency may request additional documents (receipts, certificates, etc.) to support your claims.

Unlike a notice of assessment, a pre-assessment review has no final legal standing and does not represent the final amount payable or refundable.

What does a notice of assessment look like?

A notice of assessment is typically a one- to two-page official document issued by the CRA or Revenu Quebec. It follows a standardized layout and includes several clearly defined sections.

At the top of the page, you'll find your name (or business name), tax year, and a unique notice of assessment number. The main body summarizes the assessment results, including the amount owing or refunded, applied credits, and any adjustments. Toward the bottom, the notice lists explanations for changes, instalment information, and important deadlines.

Whether issued federally or provincially, the structure is consistent, which makes it easier to review and compare with your original tax return.

Does a notice of assessment mean you owe money?

Not necessarily. A notice may show an amount owing, a refund, or a zero balance. It all depends on the tax assessment performed by the authorities.

Is a notice of assessment the same as a T4 slip?

No. A notice of assessment and a T4 slip are very different tax documents, both in purpose and origin.

The T4 is an income slip issued by an employer. It shows wages paid and source deductions for a given year. It serves as a reference to file a tax return but does not constitute a tax decision.

A notice of assessment, on the other hand, is an official document issued by the Canada Revenue Agency (CRA) or Revenu Quebec after processing a tax return. It confirms the tax calculated, credits accepted or denied, any adjustments made, and the final balance payable or refundable.

Frederic Roy-Gobeil

CPA, M.TAX

Body

Passionate about entrepreneurship and taxation, Frédéric Roy-Gobeil is President and Founder of T2inc.ca, an online platform dedicated to tax and accounting management for Canadian SMEs. With a solid expertise in corporate taxation, he has also contributed to the creation of numerous start-ups, including Delve Labs.

As an author and content creator, he regularly shares his knowledge through articles and videos on taxation, accounting and financial independence. His goal: to help entrepreneurs better understand their tax obligations and maximize the profitability of their business.

Connect with Frédéric:

In this article

- What Is a Notice of Assessment (NOA)?

- Where to Find Your Notice of Assessment

- How To Find Your Notice Of Assessment Number

- Understanding Your Federal Or Provincial Notice Of Assessment

- Be Careful With An Arbitrary Notice Of Assessment

- How to Dispute a Notice of Assessment from the CRA or Revenu Quebec

- T2inc.ca Supports You With Your Tax Obligations

- FAQ – Notice of Assessment in Canada

Contact our experts

Have a question? Need help? Fill out our online form to get help from our experts.

Contact usRelated articles

Need more help?

Contact us by filling out our form

Are you interested in our services, but would like more information before taking the plunge? Contact us today and one of our tax accountants will be in touch to help you.

At T2inc.ca, we're committed to helping business owners manage their company's tax affairs so they can grow their business.